Last updated: May 11, 2026

Quick Answer

Cursor AI (built by Anysphere) reached a $50B+ pre-money valuation in April 2026, nearly doubling its $29.3B valuation from just five months earlier [1][2]. The company hit $2B in annualized recurring revenue (ARR) by February 2026 and is forecast to reach $6B ARR by year-end, making it the fastest-scaling B2B SaaS product in history. A potential $60B acquisition option from SpaceX further signals extraordinary market confidence in AI-powered coding tools [8].

Key Takeaways

- Cursor’s valuation jumped from $29.3B (November 2025) to $50B+ (April 2026) in under six months [2][6]

- ARR grew from $1M in December 2023 to $2B by February 2026, with $6B projected by end of 2026 [2][3]

- A $2B funding round led by Andreessen Horowitz and Thrive Capital, with Nvidia participating, was in advanced talks as of April 2026 [1]

- SpaceX announced a $10B collaboration with a $60B acquisition option [8]

- Cursor achieved positive gross margins through its proprietary Composer model and cheaper inference costs [2]

- Key competitors include GitHub Copilot ($10/mo), Claude Code, Windsurf ($15/mo), and OpenAI Codex

- Critics argue the $50B valuation represents a 25x revenue multiple, which may be unsustainable

- A critical Git RCE vulnerability was patched in May 2026, raising questions about security at scale [7]

How Did Cursor AI Reach a $50B Valuation So Quickly?

Cursor’s valuation trajectory is unprecedented in enterprise software. The company went from a $1M ARR startup in late 2023 to commanding a $50B+ valuation by April 2026, a timeline that compressed what typically takes a decade into roughly 28 months [2][5].

The growth milestones tell the story:

| Date | ARR | Valuation |

|---|---|---|

| December 2023 | $1M | Undisclosed |

| June 2025 | $500M | Undisclosed |

| November 2025 | $1B | $29.3B (Series D) |

| February 2026 | $2B | — |

| April 2026 | — | $50B+ (new round) |

| End of 2026 (forecast) | $6B | TBD |

Three factors drove this acceleration:

- Enterprise adoption surge. Large organizations moved from individual developer licenses to company-wide deployments, creating predictable, high-value contracts.

- Proprietary model economics. Cursor’s Composer model (launched November 2025) reduced dependence on expensive third-party AI providers like Anthropic, flipping gross margins positive [2].

- Agentic coding capabilities. Cursor’s multi-file editing and autonomous task completion outperformed simpler autocomplete tools, justifying premium pricing.

SaaStr called Cursor “the fastest B2B to scale ever,” noting it hit $1B ARR faster than even OpenAI. For context, Slack took about 5 years to reach $1B ARR. Cursor did it in roughly 17 months from meaningful revenue.

If you’re interested in how AI is reshaping creative workflows beyond coding, our comprehensive guide to AI-powered content generation tools covers the broader landscape.

What’s Driving the $2B Funding Round?

The funding round, led by Andreessen Horowitz and Thrive Capital with Nvidia and potentially Battery Ventures participating, would raise over $2B at a $50B+ pre-money valuation [1][3]. This nearly doubles the $29.3B valuation from the Series D just five months prior [6].

Why investors are paying this premium:

- Revenue velocity. Tripling from $2B to $6B ARR within a single year (if achieved) would justify high forward multiples.

- Market size. The global developer tools market is enormous, and AI coding assistants are becoming as essential as IDEs themselves.

- Margin improvement. Moving to proprietary models means Cursor keeps more of each dollar earned, rather than passing it to API providers [2].

- Enterprise stickiness. Once teams integrate Cursor into their workflows, switching costs are substantial.

Nvidia’s participation is notable because it signals hardware-layer confidence in Cursor’s compute needs and growth trajectory. When your GPU supplier invests in your company, it suggests they see sustained demand ahead.

Decision rule: If you’re evaluating AI coding tools for enterprise deployment in 2026, Cursor’s financial backing and enterprise focus make it a lower-risk vendor choice compared to smaller competitors, but expect pricing to reflect that premium positioning.

The AI-powered content optimization guide on our site explores similar dynamics in how AI tools are reshaping professional workflows.

How Does the SpaceX Deal Change the Picture?

On April 21, 2026, SpaceX announced a $10B collaboration with Cursor for AI coding and knowledge work, leveraging its Colossus supercomputer. The deal includes an option to acquire Cursor for $60B later in 2026 [8].

This is significant for several reasons:

- Validation at the highest level. SpaceX choosing Cursor over alternatives (including Microsoft-backed GitHub Copilot) signals product superiority in complex engineering environments.

- Acquisition premium. The $60B option represents a 20% premium over the $50B funding valuation, suggesting SpaceX sees further upside.

- Microsoft passed. Reports indicate Microsoft explored acquiring Cursor but ultimately didn’t proceed, possibly due to its existing GitHub Copilot investment [8].

What this means for developers: If SpaceX engineers building rocket software trust Cursor for mission-critical code, it sets a credibility benchmark that few competitors can match.

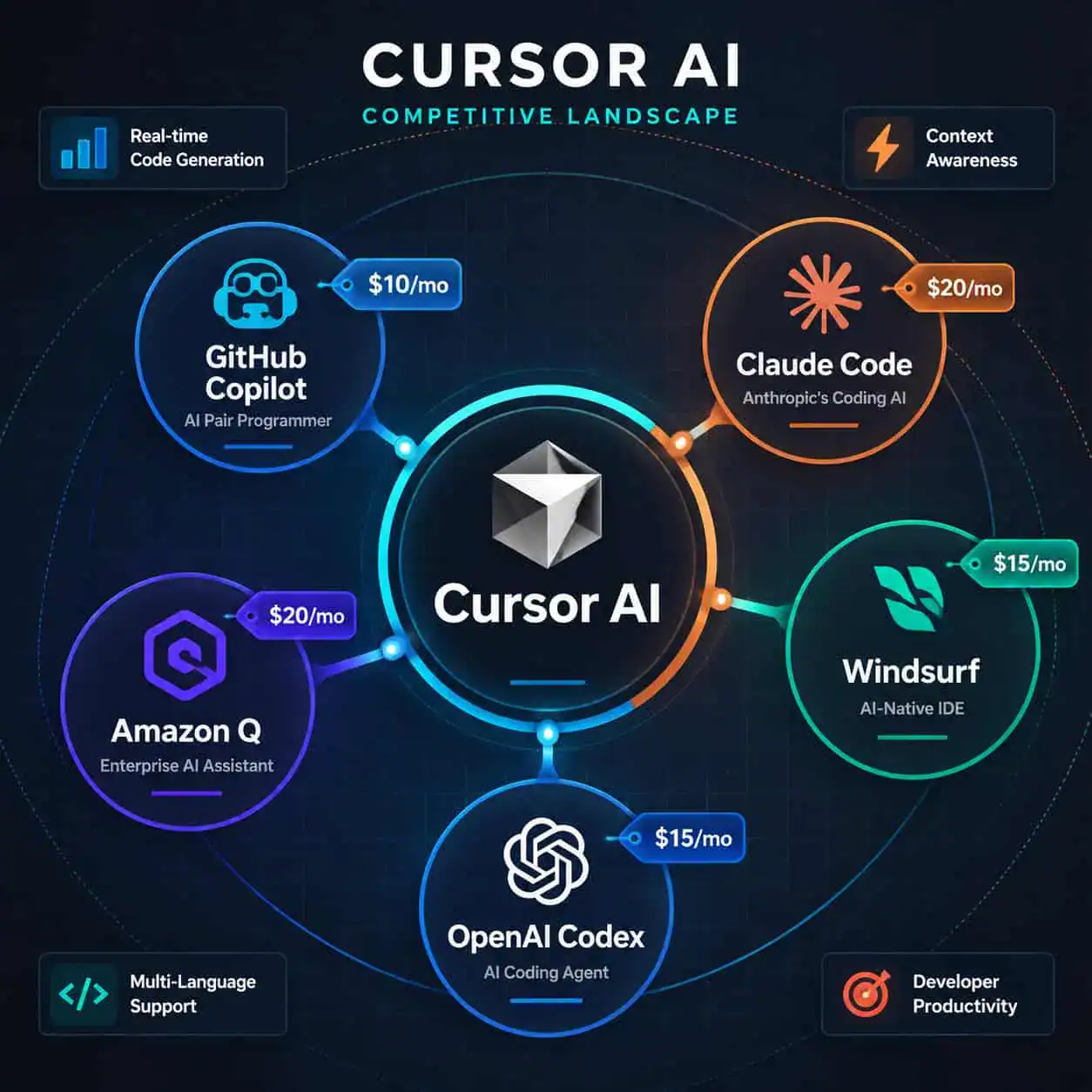

How Does Cursor Compare to Competitors in 2026?

Cursor leads the AI coding assistant market in agentic capabilities, but faces real competition on price and specific use cases.

| Tool | Price | Key Strength | Weakness |

|---|---|---|---|

| Cursor | $20/mo Pro, $40/seat Business | Multi-file agentic editing | Opaque credit system, expensive |

| GitHub Copilot | $10/mo | Ecosystem integration, price | Less capable at complex tasks |

| Claude Code | Usage-based | Terminal-based agents, reasoning | No IDE integration |

| Windsurf | $15/mo Pro | Price/performance balance | Smaller user base |

| Amazon Q | Included with AWS | AWS integration | Limited outside AWS |

| OpenAI Codex | Usage-based | Multi-step task completion | Newer, less proven |

Choose Cursor if: You need autonomous multi-file editing, work on complex codebases, and your organization can justify $40/seat for productivity gains.

Choose Copilot if: You want the cheapest reliable option with tight GitHub/VS Code integration and don’t need agentic features.

Choose Claude Code if: You prefer terminal-based workflows and value reasoning quality over IDE polish.

One common mistake: assuming all AI coding tools are interchangeable. Cursor’s strength is specifically in agentic workflows where the AI modifies multiple files, runs tests, and iterates. For simple autocomplete, cheaper options work fine.

For teams building websites without deep coding expertise, our guide to no-coding website design platforms covers alternatives that complement AI coding tools.

Is Cursor AI Overvalued at $50B?

This is the central debate. At $2B ARR with a $50B valuation, Cursor trades at roughly 25x revenue. That’s expensive by any SaaS standard, though the growth rate (tripling annually) partially justifies it [2][4].

Arguments that $50B is justified:

- Revenue is tripling year-over-year

- Gross margins are improving with proprietary models

- Total addressable market (all developers globally) is massive

- Enterprise contracts provide revenue predictability

Arguments that it’s overvalued:

- 25x ARR multiples historically compress as growth slows

- Competitors (especially Anthropic and OpenAI) have deeper AI research capabilities

- Pricing controversies (the August 2025 credit system shift caused user backlash)

- Some viral developer sentiment suggests momentum may be stalling as Claude Code gains traction

LinkedIn analyst Josh Schachter directly questioned whether $2B+ ARR warrants a $50B valuation, calling it potentially overvalued despite enterprise dominance.

Edge case to watch: If Cursor’s $6B ARR forecast materializes by end of 2026, the current valuation looks more reasonable at roughly 8x forward revenue. If growth decelerates, the multiple becomes harder to defend.

What Are the Risks to Cursor’s Financial Trajectory?

Despite the impressive numbers, several risks could derail Cursor’s trajectory:

- Supplier risk. While Cursor has its Composer model, it still relies on third-party LLMs for some features. If Anthropic or OpenAI restrict access or raise prices, margins could compress.

- Security concerns. The May 2026 Git RCE vulnerability (patched in version 2.5) showed that AI agents executing code create novel attack surfaces [7]. Enterprise buyers care deeply about this.

- Pricing backlash. The shift to opaque credit-based pricing in 2025 frustrated individual developers. If enterprise buyers face similar surprises, churn could increase.

- Competition intensifying. OpenAI’s revamped Codex, Anthropic’s Claude Code, and Google’s offerings are all improving rapidly.

- Market concentration. Heavy reliance on enterprise contracts means losing a few large customers could materially impact revenue.

Cursor open-sourced its coding agent engine in early May 2026, which helps address transparency concerns but also gives competitors a roadmap [7].

For those building AI-integrated products, understanding how to integrate AI-powered chatbots provides useful context on the broader AI integration landscape.

What Does Cursor’s Growth Mean for the Developer Tools Market?

Cursor’s trajectory signals a fundamental shift: developer tools can now scale like consumer apps while charging enterprise prices. This has implications for anyone building or buying software tools.

For developers: AI coding assistants are becoming non-optional. The productivity gap between developers using these tools and those who don’t is widening.

For investors: The AI coding space is attracting massive capital. Expect more competition and eventual market consolidation.

For enterprises: Budget for AI coding tools as infrastructure, not optional perks. The ROI at $40/seat is clear if developers ship 20-30% faster.

The best AI graphic design tools and Figma AI workflow automation resources show similar AI-driven productivity gains happening across creative disciplines.

Conclusion

Cursor AI’s financial trajectory from $1M ARR to a $50B+ valuation in under three years represents something genuinely new in enterprise software. The combination of explosive revenue growth, improving margins through proprietary models, and strategic partnerships (particularly the SpaceX deal) creates a compelling narrative for continued growth.

Actionable next steps:

- If you’re evaluating Cursor for your team: Start with Pro ($20/mo) to test agentic capabilities before committing to Business tier. The multi-file editing is where the real value lives.

- If you’re an investor or analyst: Watch the $6B ARR target closely. Q3 2026 earnings signals will determine whether the 25x multiple holds.

- If you’re a competitor: Cursor’s open-sourcing of its agent engine creates an opportunity to build on proven architecture rather than starting from scratch.

- If you’re a developer choosing tools: Try Cursor alongside Claude Code and Copilot on your actual codebase. The best tool depends on your workflow (IDE-centric vs. terminal-centric) and budget.

The valuation debate will ultimately be settled by execution. If Cursor delivers $6B ARR by December 2026, the $50B price tag will look prescient. If growth decelerates, it’ll join the list of AI companies that raised at peak hype.

FAQ

What is Cursor AI’s current valuation in 2026? As of April 2026, Cursor is in talks for a funding round at over $50B pre-money valuation, up from $29.3B in November 2025 [1][2].

How much revenue does Cursor AI generate? Cursor reached $2B in annualized recurring revenue by February 2026, with forecasts of $6B ARR by end of 2026 [2][3].

Who are Cursor AI’s main investors? The latest round is led by Andreessen Horowitz and Thrive Capital, with Nvidia and potentially Battery Ventures participating [1].

What is the SpaceX-Cursor deal? SpaceX announced a $10B collaboration using its Colossus supercomputer, with an option to acquire Cursor for $60B later in 2026 [8].

How much does Cursor cost? Pro plan is $20/month (500 premium requests), Business is $40/seat/month. Individual developers may find the credit system limiting.

Is Cursor AI profitable? Cursor achieved positive gross margins after launching its proprietary Composer model in November 2025, though full profitability status hasn’t been disclosed [2].

How fast has Cursor grown? From $1M ARR in December 2023 to $2B ARR in February 2026, roughly 2,000x growth in 26 months. SaaStr calls it the fastest B2B scale ever.

What happened with the Cursor security vulnerability? In May 2026, a critical Git RCE vulnerability was patched in version 2.5. Malicious repositories could trigger arbitrary code execution via Cursor’s AI agent. No in-the-wild exploits were reported [7].

Did Microsoft try to buy Cursor? Reports indicate Microsoft explored acquiring Cursor but passed, possibly due to its existing investment in GitHub Copilot [8].

Is Cursor AI overvalued? At 25x current ARR ($50B / $2B), it’s expensive. But if the $6B forecast holds, forward multiples drop to roughly 8x, which is more reasonable for a company tripling annually.

References

[1] Cursor Ai 2 Billion Funding Round – https://www.cnbc.com/2026/04/19/cursor-ai-2-billion-funding-round.html [2] Sources Cursor In Talks To Raise 2b At 50b Valuation As Enterprise Growth Surges – https://techcrunch.com/2026/04/17/sources-cursor-in-talks-to-raise-2b-at-50b-valuation-as-enterprise-growth-surges/ [3] Ai Coding Startup Cursor In Talks To Raise 2 Billion In Funding – https://www.bloomberg.com/news/articles/2026-04-17/ai-coding-startup-cursor-in-talks-to-raise-2-billion-in-funding [4] Ai Coding Startup Cursor Seeks 115735149 – https://finance.yahoo.com/sectors/technology/articles/ai-coding-startup-cursor-seeks-115735149.html [5] Cursor Anysphere 2b Funding 50b Valuation Ai Coding – https://techfundingnews.com/cursor-anysphere-2b-funding-50b-valuation-ai-coding/ [6] Series D – https://cursor.com/blog/series-d [7] Cursor News May 2026 – https://blog.mean.ceo/cursor-news-may-2026/ [8] Spacex Strikes 60 Billion Deal Cursor – https://fortune.com/2026/04/22/spacex-strikes-60-billion-deal-cursor/